Business Cash Advance vs Bank Loan

Many small business owners in the UK find themselves frustrated with bank loan models because the timing, security, or cash flow impact does not quite fit. When you are weighing up “business cash advance vs bank loan”, the structure of the funding can matter more than the headline rate.

Here we break down, in plain English, how a traditional loan compares to Funding Alternative’s Business Cash Advance so you can see which better supports your cash flow and your approval chances.

Business Cash Advance vs Bank Loan in Simple Terms

Before we place Business Cash Advance (BCA) and bank loans head-to-head, it helps to understand how finance jargon translates into day-to-day business.

Security (Collateral)

- Bank Loan: Often secured against property or assets, with a personal guarantee typically required. If things go wrong, those assets are at risk.

- Business Cash Advance: Unsecured Cashflow Finance focused more on your revenue and bank data, not on property or assets, though a personal guarantee is required.

Term (How long you repay)

- Bank Loan: A bank loan usually has a fixed term, often 2–5 years. It has the same monthly repayment due, regardless of how your business trading month went.

- Business Cash Advance: A Business Cash Advance is designed as shorter-term funding. It is typically repaid over months rather than years.

Fees, Interest, and Total Cost

- Bank Loan: Interest-based. You see an Annual Percentage Rate (APR), but the total you repay depends on how long you hold the loan, whether rates move, and any early repayment or arrangement fees.

- Business Cash Advance: No interest. You agree to a fixed fee upfront, so the total repayable is known from day one and does not change over time.

Repayment Method

- Bank Loan: Fixed monthly instalments by direct debit. The same amount leaves your account each month, even if it has been a slow trading period.

- Business Cash Advance: Repayments can be structured as fixed daily or weekly amounts, or as a percentage of your incoming receipts tracked via open banking, alongside a minimum weekly amount.

How Repayments Hit Your Cash Flow

The way money leaves your account can matter more than the total cost on paper.Fixed Monthly vs Fixed Daily or Weekly

With a bank loan, the repayment is usually a single, fixed monthly sum. That direct debit goes out on the same date, whether it’s your busiest or quietest month. Miss one or two payments, and you can quickly find yourself in arrears, dealing with letters and calls instead of customers.

The onus is on you to make sure the cash is ready and waiting before the debit strikes.

With a Business Cash Advance from Funding Alternative, you can choose fixed daily or weekly repayments instead. These smaller, more frequent amounts are set from the start and remain consistent, which can be easier to plan around than one large monthly hit.

Many owners find that spreading the burden across the month makes the mental load and cash flow impact lighter.

Revenue-Based Repayments Tracked via Open Banking

When revenue swings more sharply, the revenue-based option can be even more forgiving. A portion of your incoming sales is used to repay the advance, which is tracked directly through your bank transactions, along with a minimum weekly amount.

When trade is strong, you clear more of the balance; when trade is weaker, you pay less that week.

You still repay the agreed fixed fee overall, but the pattern shares more of the short-term risk between you and the funder. We find this is particularly apt in sectors such as hospitality, certain types of retail, construction, automotive, IT services, transport and logistics.

A Side-by-Side Look at Business Cash Advance versus Bank Loan

| Feature | Traditional Bank Loan | Funding Alternative Business Cash Advance |

| Approval Speed | Commonly, 2–8 weeks from full application to payout. | Pre-approvals are issued within 4 hours of receiving the minimum information. |

| Repayment Method | Fixed monthly instalments over a multi-year term. | Fixed daily/weekly repayments or revenue-based repayments with a minimum weekly amount. |

| Cost Structure | Interest-based (APR); the total cost can rise if the term extends or the rate changes. | Fixed fee business funding; total repayable agreed upfront, no interest accrual. |

| Flexibility | Less flexible, early settlement charges may apply, and rescheduling can be slow. | Short-term, with options to adjust or top up if performance supports it. |

| Eligibility | Strong credit scores and excessive security are often required. | Suits SMEs with weaker credit or limited assets, assessed primarily on cash flow and trading history. |

| Complexity | Requires extensive documentation and underwriting processes. | Streamlined application, minimal paperwork, and quick decision-making. |

| Personal Credit Record | Heavily relied upon; poor personal credit can significantly impact approval. | Considered, but less emphasis; focus is more on business performance and cash flow. |

| Business Track Record/Phoenix | Requires established trading history. Phoenix businesses often declined. | Can accommodate shorter trading histories. Phoenix businesses may be considered depending on recent performance. |

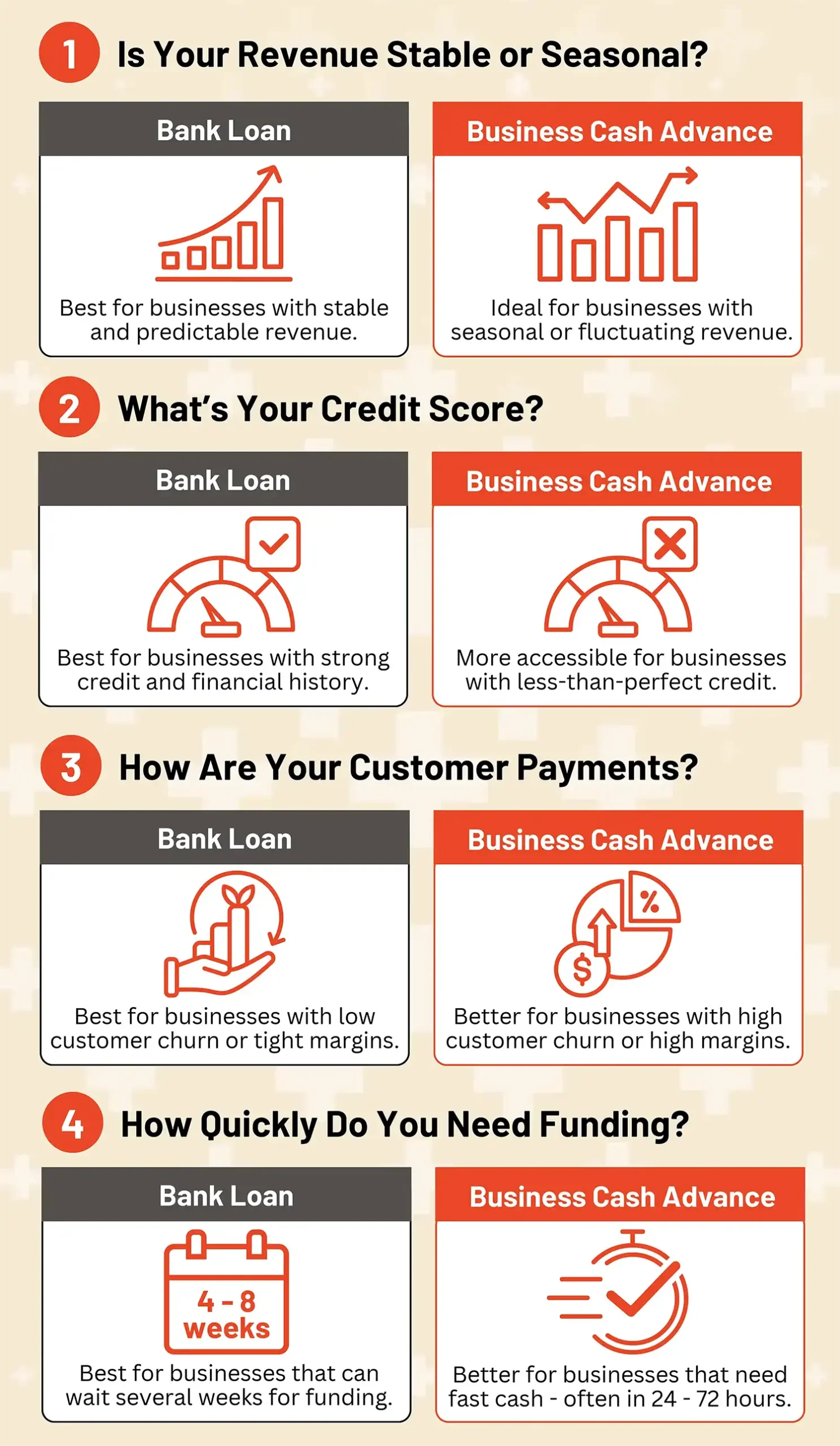

A bank loan is often the lowest headline-cost option if you have time, strong security, and stable income.

Business Cash Advance prioritises speed, eligibility, and transparency for SMEs that value certainty and short-term support.

When a Bank Loan Makes Sense

A bank loan absolutely has its place. It can be the right tool when:

- You are funding a long-term investment, such as buying property, major equipment, or a full refurbishment that will pay back over many years.

- Your revenue is relatively stable and predictable, so a fixed monthly repayment is not a strain.

- You have strong credit and are comfortable offering security to access potentially lower long-term costs.

- You have the time and headspace to work through a more detailed application and wait weeks rather than days for a decision.

In those situations, it is perfectly reasonable to explore bank options first, then look at alternatives for shorter-term or more tactical cash flow needs.

When a Business Cash Advance Provides a Clear Advantage

A Business Cash Advance comes into its own when reality is messier than a spreadsheet.

It is often a better fit if:

- Your revenue is seasonal or fluctuating, and a large monthly repayment could push you into an overdraft during a quiet month.

- You have been turned down by a bank, or you know your journey hasn’t been perfect, and your credit doesn’t tell the full story. We understand that building a business comes with ups and downs. Setbacks, past credit issues, or complex histories don’t define where you are today. What matters is your current performance and the strength of your business now — not a “perfect” past.

- You need a decision and funds quickly to deal with taxes, payroll, suppliers, or to grab a growth opportunity.

- You prefer a partner-like structure without taking equity: unsecured funding that behaves more like flexible, situational capital than a rigid traditional loan.

- You value seeing the full cost as a fixed fee upfront, rather than trying to model APRs across different terms.

Funding Alternative’s Business Cash Advance is exactly this kind of cash flow finance for SMEs.

Our unsecured, flexible repayment options (fixed daily/weekly or revenue-based via open banking), and clear fixed-fee structure show you where you stand.

Loan vs Cash Advance (Hypothetical Examples)

These are illustrative examples only, based on the common patterns that we see.

The restaurant that chose a Business Cash Advance

A small restaurant has good reviews and loyal customers, but takings swing by 30–40% between quiet winters and busy summers. A looming VAT bill and a broken oven hit at the same time. The bank is willing to talk but estimates four to six weeks for a final decision.

Instead, the owner takes a Business Cash Advance. Funds arrive quickly, and repayments are linked to incoming receipts with a minimum weekly amount. In busy weeks, they clear more of the balance; in quieter weeks, less leaves the account, keeping staff and suppliers paid without slipping into arrears.

The engineering firm that chose a bank loan.

A light engineering firm has multi-year contracts with large, reliable customers and owns its premises. It wants to buy a new machine that will be used for the next decade. Cash flow is steady and predictable.

In this case, a secured bank loan over five years gives them a relatively low monthly repayment and a competitive interest rate. The approval takes longer, but they can plan around it. For them, the bank loan is the right tool, and they only consider alternatives later if they need short-term working capital to bridge specific projects.

Quick Checklist: Which Route Should You Explore First?

Use this as a simple sense-check:

If you are in the grey area between those answers, that is normal. It just means a short conversation will likely save you time and second-guessing. You can always chat with a Funding Alternative expert here.

Funding Alternative: Equity-Like Support Without Taking Equity

Our role is straightforward: help you match your situation to the funding that does the most good. We specialise in unsecured Business Cash Advances for UK SMEs, with flexible repayment models tracked via open banking and a fixed-fee structure that makes planning easier.

We know good businesses get told “no” by banks for reasons that do not always reflect what is happening on the ground. We step in as situational capital, so you keep control of your business while smoothing the bumps in your cash flow.

If you are comparing a business cash advance to a bank loan and want a straight, jargon-free view of what might fit best, we are here to help.

We will walk you through the pros and cons for your specific position so you can decide with confidence, not pressure.